Portfolio Review

Frasers Commercial Trust's properties are located in Singapore and Australia.

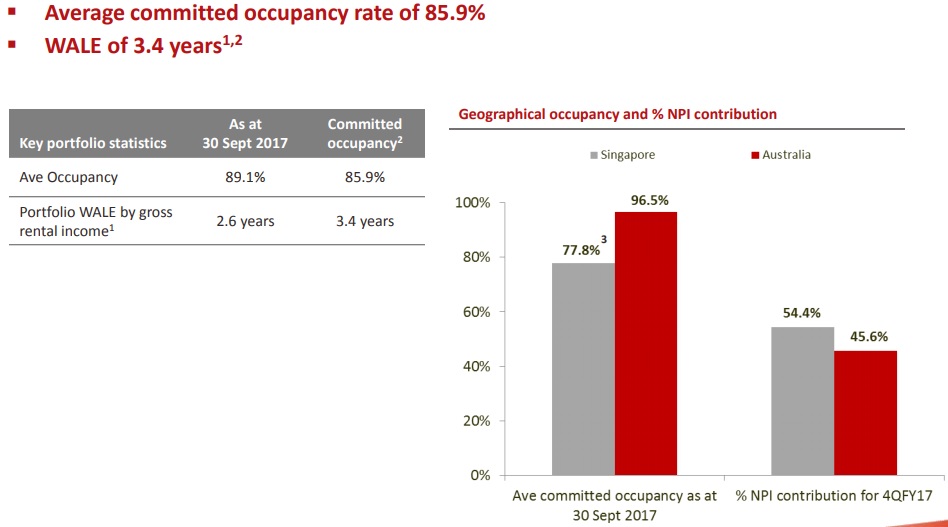

The lower occupancy rate is actually due to planned construction works for Hotel and Commercial Project at China Square Central. China Square Central is the largest contributor in FCOT's portfolio. However, the next slide does look worrying. Over 30% of portfolio lease expiry by gross rental income in 2018. It is already known news that HP Enterprise Singapore will not be renewing their lease at Alexandra Technopark. It does looks like a challenger year for FCOT in 2018.

Let's delve deeper into their lease expiry profile. Alexandra Technopark's lease expiry seems to be of greatest concern here. According to a Straits Times article published on Oct 20, FCOT was still in talks with HPS on the lease expiry. Wasn't that a bit too late? According to this article, HPS contributed 11.1% of FCOT's gross rental income. Link to article here.

Let's look at FCOT's rental reversion. Overall, it's positive for FY2017. China Square Central's negative rental reversion is caused by their construction works.

37% of FCOT's leases have step up rents in 2018.

Alexandra Technopark's current AEI is due to complete in mid 2018. Hopefully, the rental yield could increase further after that.

Construction works at China Square Central is due to be completed by mid 2019. Wow. A long wait.

My Thoughts

There's 1 thing I like about FCOT is they have a distribution reinvestment plan. When their share price drops, I can opt to receive dividend in the form of Units. This helps me to save me on commission fees.The downside is I ended up having odd lots. However, I plan to keep this REIT for longterm so this is not much of an issue to me. However, for those interested in investing in this REIT, do take note of their lease expiry profile in 2018.

Other Stuff that I Like:

Gearing: 34.7% (Healthy)

NAV: 1.58 (Trading below NAV. Current Price as at 24th Nov's Closing: 1.43.)

Steady Growing Dividend. Dividend Yield based 24th Nov's Closing Price: 9.82/1.43 = 6.87%

(I am getting more based on my purchase price)

Screenshot from Stocks.Cafe. Management has the capability to grow the DPU.

This concludes my blog post on FCOT's 4QFY17 Financial Results. The link to the actual report could be found at the link here if you are interested.

Stay Tune for this Upcoming Post: Is the Soil Still Fertile For This REIT?